With increased global tax scrutiny and information exchange between countries, tax residency status has become a critical issue for individuals living, working, or investing in the UAE. Obtaining a UAE Tax Residency Certificate (TRC) can play a decisive role in accessing Double Taxation Avoidance Agreement (DTAA) benefits and managing cross-border tax exposure.

This guide explains UAE tax residency rules for individuals, the eligibility criteria for a Tax Residency Certificate, and key compliance considerations under the UAE tax framework.

Table of Contents

What Is Tax Residency in the UAE?

Tax residency determines which country has the right to tax an individual’s income. In the UAE, tax residency for individuals is governed by Cabinet Decision No. 85 of 2022, which sets out objective criteria for determining residency status.

An individual may be treated as a UAE tax resident even though the UAE does not levy personal income tax.

Who Is Considered a UAE Tax Resident?

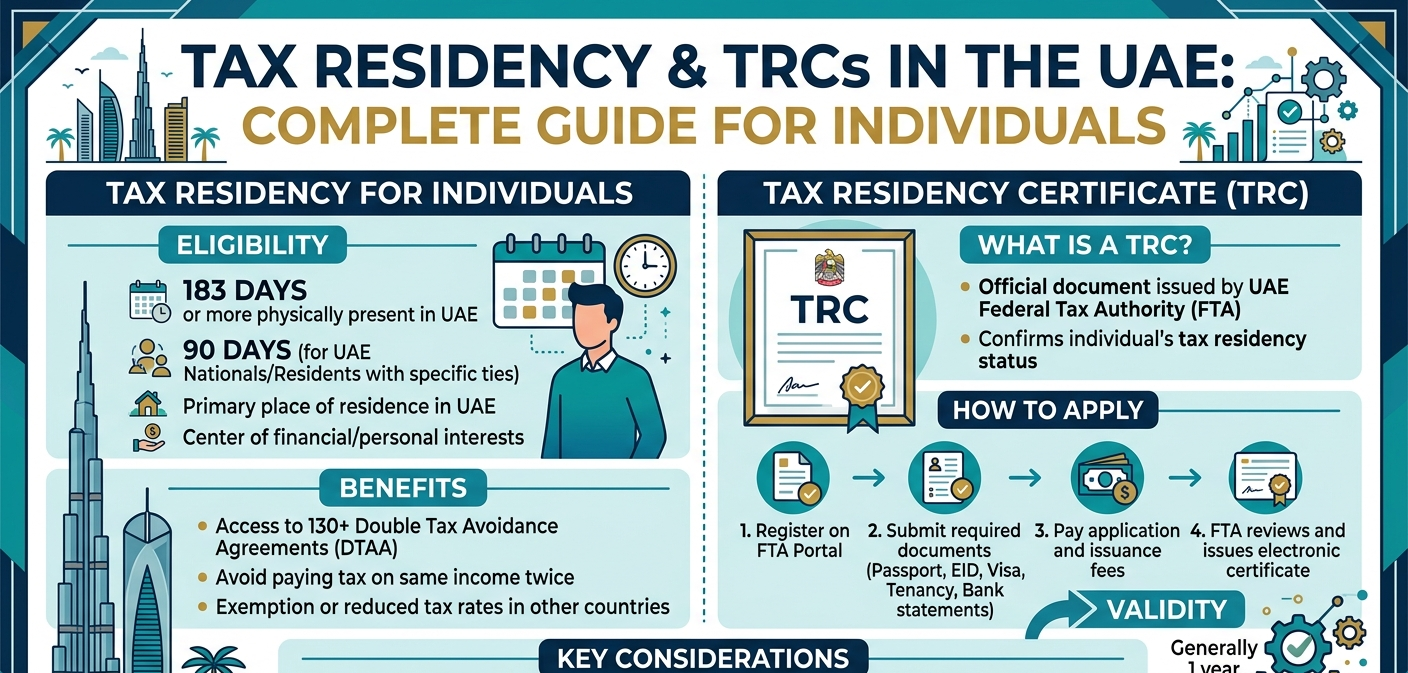

An individual may qualify as a UAE tax resident if any one of the following conditions is met:

- The individual’s usual or primary place of residence is in the UAE

- The individual is present in the UAE for 183 days or more in a consecutive 12-month period

- The individual is present in the UAE for 90 days or more and:

- Is a UAE national or resident, or

- Conducts business or employment activities in the UAE

Meeting these conditions allows the individual to be recognised as a tax resident of the UAE for treaty purposes.

What Is a Tax Residency Certificate (TRC)?

A Tax Residency Certificate (TRC) is an official document issued by the UAE Ministry of Finance (MoF) confirming that an individual is a tax resident of the UAE for a specific financial year.

The TRC is primarily used to:

- Claim DTAA benefits

- Avoid or reduce double taxation

- Provide proof of tax residency to foreign tax authorities

Eligibility for a UAE TRC (Individuals)

To apply for a TRC, an individual must generally:

- Hold a valid UAE residence visa

- Meet the tax residency criteria under Cabinet Decision No. 85 of 2022

- Demonstrate physical presence in the UAE

- Have a residential address in the UAE

- Maintain supporting documentation such as bank statements and tenancy contracts

Each TRC is issued for a specific tax year and is not automatically renewable.

Documents Required for a TRC Application

Commonly required documents include:

- Passport and UAE residence visa

- Emirates ID

- Entry and exit report

- Tenancy contract or proof of residence

- UAE bank statements

- Salary certificate or proof of income (where applicable)

The Ministry of Finance may request additional documents based on individual circumstances.

Why Is a TRC Important for Individuals?

A UAE TRC is particularly important for individuals who:

- Earn income from foreign jurisdictions

- Hold overseas investments or directorships

- Are subject to tax residency challenges in another country

- Wish to access DTAA relief on dividends, interest, royalties, or capital gains

Without a TRC, foreign tax authorities may deny treaty benefits, even if the individual resides in the UAE.

Common Mistakes Individuals Make

- Assuming a UAE residence visa automatically grants tax residency

- Not tracking physical presence days accurately

- Applying for a TRC without meeting eligibility criteria

- Using outdated or incomplete documentation

- Ignoring tax residency risks in the home country

These mistakes can lead to rejection of the TRC application or disputes with foreign tax authorities.

Key Takeaways

- UAE tax residency is determined by objective legal criteria

- Individuals may qualify without paying personal income tax

- A TRC is essential for claiming DTAA benefits

- Physical presence and documentation are critical

- Proper planning avoids cross-border tax disputes.