The UAE is widely recognised for its tax-efficient personal and investment environment. Unlike many jurisdictions, the UAE does not levy personal income tax, and this extends to capital gains, dividends, and most categories of foreign income. However, international tax exposure may still arise through foreign tax laws and Double Taxation Avoidance Agreements (DTAAs).

This guide explains the tax treatment of capital gains, dividends, and foreign income in the UAE, with a focus on legal clarity and cross-border considerations.

Table of Contents

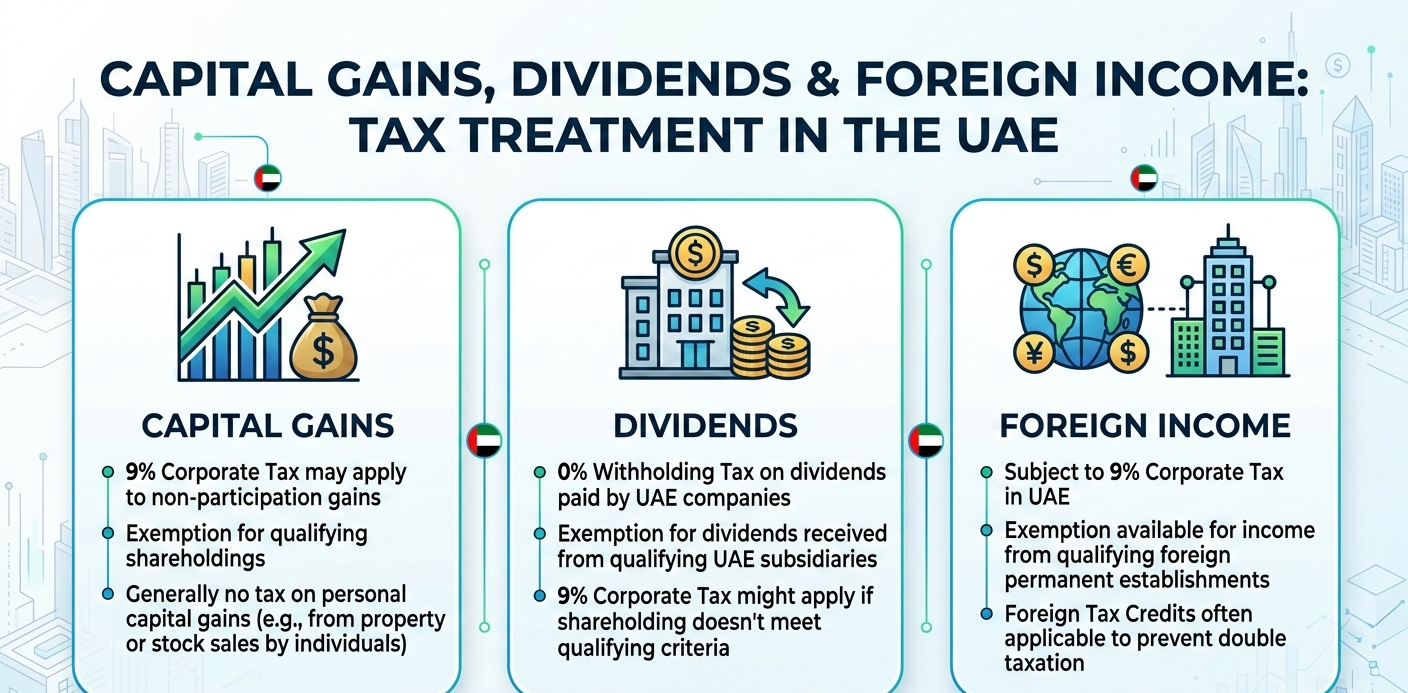

Capital Gains in the UAE

The UAE does not impose capital gains tax on individuals.

This means gains arising from the sale of:

- Shares and securities

- Real estate (subject to emirate-level transfer fees, not tax)

- Business assets held personally

- Investments and financial instruments

are not subject to taxation in the UAE.

However, capital gains may still be taxed in another jurisdiction depending on:

- The source country of the asset

- The individual’s tax residency status abroad

- Applicable DTAA provisions

Dividend Income in the UAE

Dividend income received by individuals in the UAE is not subject to tax.

This includes:

- Dividends from UAE companies

- Dividends from foreign companies

- Investment portfolio distributions

The UAE does not levy withholding tax on dividends, nor does it tax dividend receipts at the individual level.

That said, foreign-source dividends may be subject to withholding tax in the country of origin, which is where DTAA protection becomes relevant.

Foreign Income and UAE Tax Treatment

As a general rule, the UAE does not tax foreign income earned by individuals, including:

- Overseas employment income

- Foreign business income

- Rental income from foreign properties

- Foreign investment income

However, foreign income may still be taxed in the source country under its domestic tax laws.

The UAE’s role in such cases is primarily as a treaty jurisdiction, rather than a taxing jurisdiction.

Role of Double Taxation Avoidance Agreements (DTAA)

The UAE has an extensive network of Double Taxation Avoidance Agreements with multiple countries. These treaties aim to:

- Prevent double taxation of the same income

- Allocate taxing rights between countries

- Reduce or eliminate withholding taxes

- Provide certainty for cross-border income flows

To claim DTAA benefits, individuals typically need to:

- Qualify as a UAE tax resident

- Obtain a UAE Tax Residency Certificate (TRC)

- Submit the TRC to foreign tax authorities

Without a valid TRC, treaty benefits may be denied, even if the individual resides in the UAE.

Important Practical Considerations

While the UAE does not tax capital gains, dividends, or foreign income:

- Other countries may still assert taxing rights

- Exit tax, remittance-based taxation, or residency rules abroad may apply

- Incorrect assumptions can lead to foreign tax disputes

Proper tax residency planning and DTAA structuring are therefore essential.

Common Misunderstandings

- Assuming “no tax in UAE” means “no tax anywhere”

- Ignoring source-country withholding taxes

- Failing to secure a UAE TRC

- Overlooking continuing tax residency obligations in another country

These issues often arise in cross-border audits and assessments.

Key Takeaways

- The UAE does not levy capital gains tax on individuals

- Dividends are not taxed in the UAE

- Foreign income is not taxed in the UAE

- DTAA protection is crucial for managing foreign tax exposure

- A Tax Residency Certificate is central to treaty benefits