Table of Contents

Overview of the UAE Corporate Tax Regime

The introduction of Corporate Tax (CT) marks one of the most significant developments in the UAE’s fiscal framework. Implemented under Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses, the regime applies to financial years starting on or after 1 June 2023.

For decades, the UAE was widely known for its zero-tax environment for most businesses. The new regime introduces a federal corporate tax of 9% on taxable profits exceeding AED 375,000, while preserving a 0% rate for lower profit levels to support startups and small businesses.

The reform aligns the UAE with global tax standards, particularly the OECD Base Erosion and Profit Shifting (BEPS) framework, while maintaining its competitiveness as an international business hub.

Although the tax rate remains modest compared with global standards, the new regime represents a shift in compliance expectations. Businesses must now maintain proper accounting records, comply with reporting requirements, and understand the rules governing exemptions, reliefs, and free-zone benefits.

Who Is Subject to Corporate Tax in the UAE?

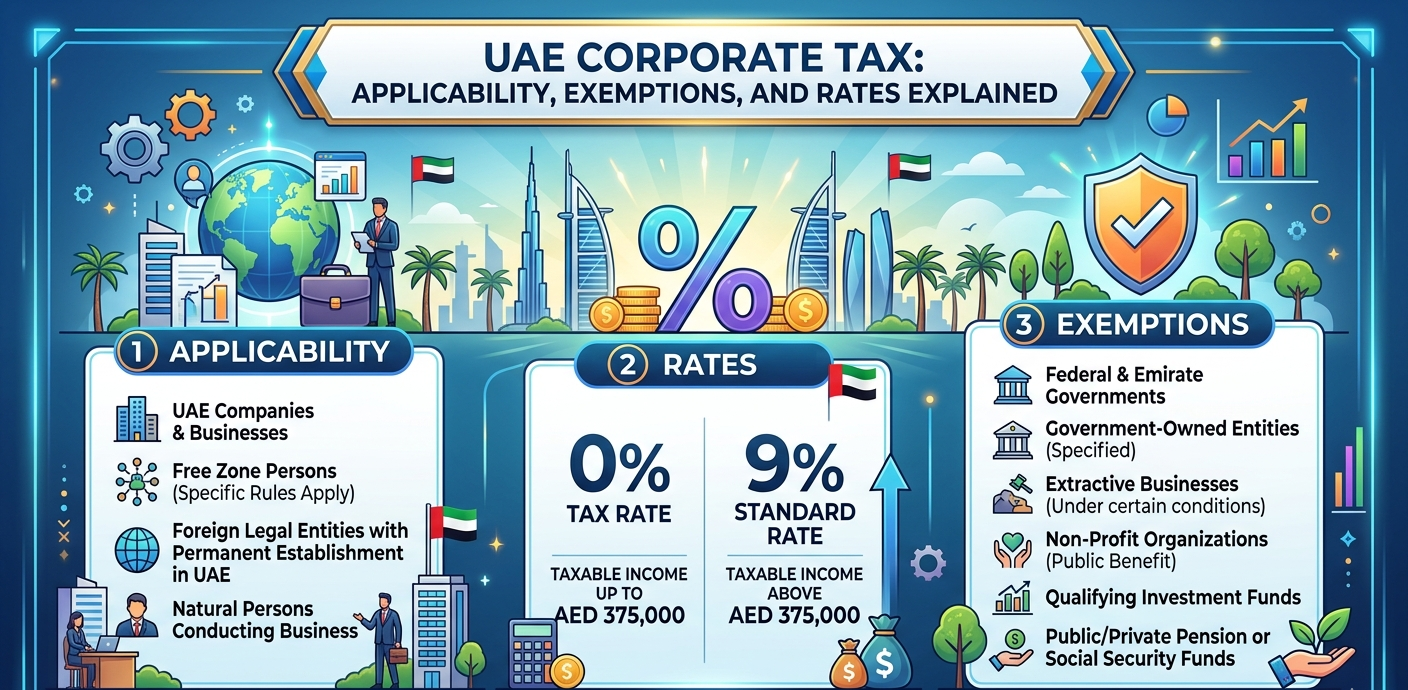

The UAE Corporate Tax regime has a broad scope, applying to most businesses operating in the country. The main categories of taxable persons include:

- UAE Resident Legal Entities

All companies incorporated or effectively managed in the UAE, including mainland and free-zone entities, are considered resident taxable persons and are generally subject to corporate tax on their worldwide income.

- Foreign Legal Entities with a UAE Presence

Foreign companies may be subject to UAE corporate tax if they:

- Have a Permanent Establishment (PE) in the UAE

- Derive UAE-sourced income

- Conduct business in the UAE through a fixed place of business or dependent agent

Tax is generally levied only on the income attributable to the UAE presence.

- Natural Persons Conducting Business

Individuals conducting business or commercial activities under a trade license in the UAE may also fall within the scope of corporate tax if their annual business turnover exceeds AED 1 million.

(This rule applies to licensed business activities, not personal income.)

- Branches and Partnerships

- Branches of foreign companies are treated as extensions of their parent entity and are generally subject to corporate tax on UAE-source income.

- Unincorporated partnerships may be treated as tax-transparent unless they elect to be treated as taxable persons.

Income Not Subject to Corporate Tax

Certain income earned by individuals remains outside the scope of corporate tax, including:

- Employment income

- Personal investment income (e.g., dividends, capital gains)

- Personal real estate income, provided it is not part of a licensed business activity

UAE Corporate Tax Rates

The UAE adopted a two-tier tax system designed to support small businesses while maintaining international competitiveness.

Standard Corporate Tax Rates

| Taxable Income | Corporate Tax Rate |

| Up to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

The 0% threshold effectively protects startups and small businesses while ensuring larger companies contribute to the tax base.

Large Multinational Groups (Pillar Two)

Multinational enterprises with global consolidated revenue of EUR 750 million or more may become subject to a minimum effective tax rate of 15% once the UAE implements the OECD Global Minimum Tax (Pillar Two) rules.

Exempt Persons Under the Corporate Tax Regime

The UAE corporate tax law exempts certain entities due to their public or social function.

Key exempt categories include:

- Government entities and government-controlled entities

- Extractive and non-extractive natural resource businesses, subject to Emirate-level taxation

- Qualifying public benefit entities (charities and non-profit organizations)

- Pension and social security funds

- Qualifying investment funds, subject to regulatory conditions

Even where tax is not payable, some exempt persons may still be required to register with the Federal Tax Authority (FTA) and maintain proper records.

How is Income Calculated for Corporate Tax?

Corporate Tax is generally calculated based on accounting net profit, as reported in the entity’s financial statements, with certain adjustments required under UAE tax law.

Key considerations include:

- Financial statements mustgenerally followInternational Financial Reporting Standards (IFRS) or IFRS for SMEs.

• Legitimate business expenses are deductible when incurred wholly and exclusively for business purposes.

• Certain expenses – such as administrative fines, penalties, and non-approved donations are non-deductible.

• Unrealised gains or losses may be excluded depending on accounting policies and tax elections.

The UAE CT framework also includes several relief mechanisms, including:

- Small Business Relief (available to businesses with revenue below AED 3 million, subject to conditions)

• Tax loss relief allowing losses to be carried forward and offset against future taxable income

• Group relief for qualifying intra-group transactions and restructuring.

Free Zone Companies: Special Tax Treatment

Free zones have historically offered tax incentives to attract foreign investment. Under the new corporate tax system, these benefits continue under specific conditions.

A free-zone entity may qualify as a Qualifying Free Zone Person (QFZP) if it meets certain requirements.

Conditions for Qualifying Free Zone Person Status

A free-zone business must:

- Maintain adequate economic substance in the free zone

- Derive qualifying income from approved activities

- Comply with transfer pricing rules and the arm’s-length principle

- Maintain audited financial statements

- Ensure non-qualifying revenue remains within the de minimis limit (lower of AED 5 million or 5% of total revenue)

Tax Rates for Free Zone Entities

If the entity qualifies as a QFZP:

- 0% tax applies to qualifying income

- 9% tax applies to non-qualifying income

Importantly, qualifying free zone persons do not benefit from the AED 375,000 0% threshold on non-qualifying income.

If the entity fails to meet the qualifying conditions, it becomes subject to the standard corporate tax regime at 9%.

Interaction with Transfer Pricing

The UAE Corporate Tax law incorporates transfer pricing rules aligned with OECD principles.

Transactions between related parties and connected persons must comply with the Arm’s Length Principle, ensuring prices reflect market conditions.

Businesses may be required to maintain:

- Transfer Pricing Disclosure Forms

• Master File and Local File documentation (depending on revenue thresholds)

Transfer pricing rules affect areas such as:

- Inter-company services

• Shared management or infrastructure

• Intra-group loans and guarantees.

Failure to comply may lead to tax adjustments and penalties.

Administrative Requirements and Deadlines

All taxable persons must register for Corporate Tax through the EmaraTax platform administered by the Federal Tax Authority.

Key obligations include:

- Maintainingbooks and records for at least 7 years

• Filing an annual corporate tax return within 9 months after the end of the financial year

• Maintaining financial statements (audited financials may be required in certain cases).

For example:

A company with a 31 December 2024 financial year end must file its Corporate Tax return by 30 September 2025.

Failure to register, file, or maintain proper records may result in administrative penalties.

Strategic Considerations for Businesses

Although the UAE remains a low-tax jurisdiction, the corporate tax regime introduces new strategic considerations for businesses and investors.

Key areas requiring attention include:

- Cross-border structuring

- Free-zone eligibility and substance requirements

- Transfer pricing compliance

- Group structuring and tax consolidation

- Proper financial reporting and record keeping

Proactive tax planning and regular compliance reviews are essential to minimize risks and maintain eligibility for available benefits.

Preparing for the UAE Corporate Tax Era

Corporate Tax in the UAE represents a significant step in the country’s transition toward a mature and internationally integrated tax system. While the rates remain among the most competitive globally, the framework emphasizes transparency, proper reporting, and compliance.

For businesses operating in the UAE, understanding the scope, exemptions, and strategic implications of corporate tax is now essential for sustainable growth and regulatory compliance.