The UAE’s corporate tax regime applies not only to companies but also to certain individuals conducting business activities. While the UAE does not impose personal income tax on salary or passive earnings, individuals who carry out licensed commercial, professional, or industrial activities may fall within the scope of corporate tax under Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses.

The determining factor is whether the individual is conducting a recognised business activity under a valid UAE licence, rather than whether they operate through a company structure.

Table of Contents

Personal Income vs Business Income: Understanding the Legal Distinction

Income earned purely in a personal capacity remains outside the corporate tax regime. This includes employment salary, dividend income, capital gains, and personal investment returns.

However, once an individual conducts an activity under a trade licence, freelance permit, or professional registration, the income generated from that activity is treated as business income. In such cases, the individual is regarded as a taxable person for corporate tax purposes.

The classification of income is therefore central to determining whether corporate tax obligations arise.

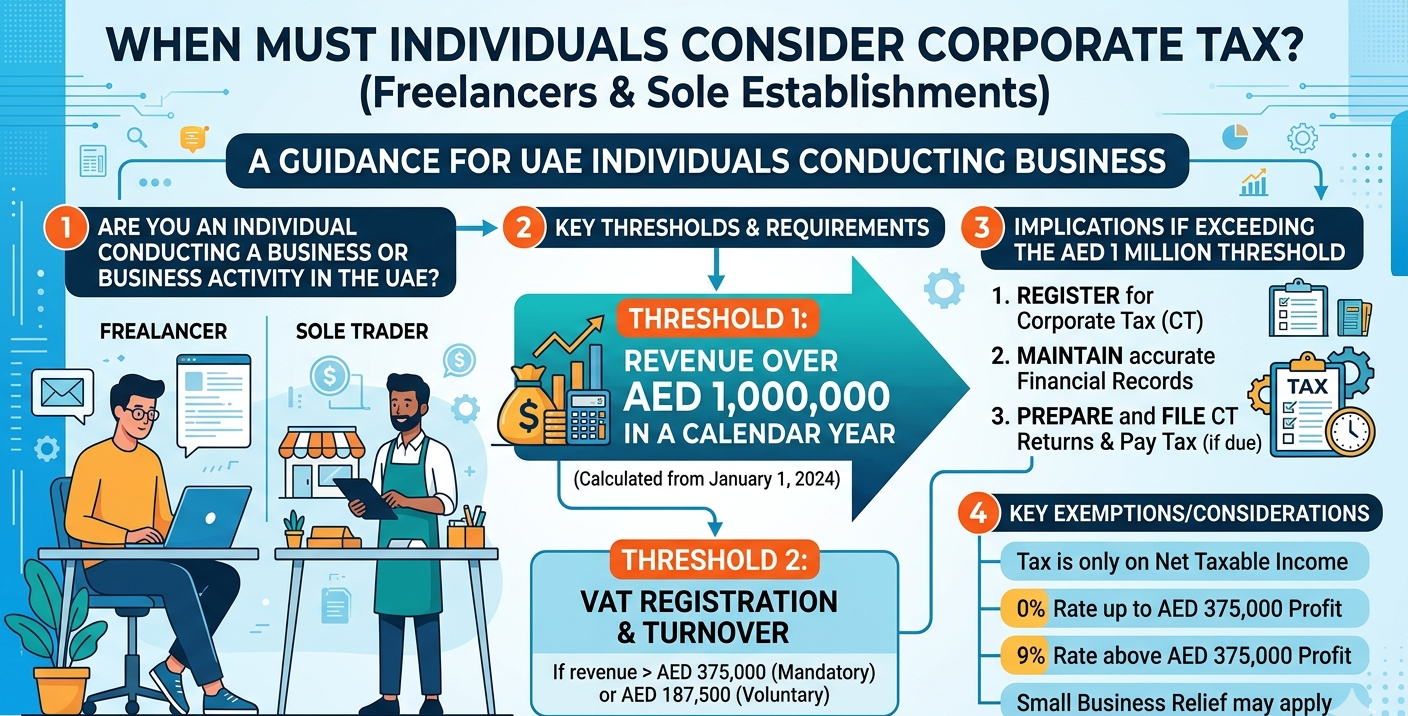

Corporate Tax Implications for Freelancers

Freelancers operating under a UAE-issued professional licence are considered to be carrying on a business activity independently. As such, they may be subject to corporate tax.

If annual taxable income exceeds AED 375,000, corporate tax is levied at 9% on the portion exceeding that threshold. Taxable income up to AED 375,000 is subject to a 0% rate.

Freelancers whose annual revenue does not exceed AED 3 million may also elect to apply for Small Business Relief, provided they meet the statutory eligibility conditions and make the appropriate election in their tax return.

Tax Treatment of Sole Establishments

A sole establishment (sole proprietorship) is owned by an individual but operates under a commercial licence. For corporate tax purposes, the income generated through the licence is treated as business income.

Where taxable profits exceed AED 375,000 in a financial year, corporate tax applies at the standard 9% rate on the excess amount. The sole establishment must register with the Federal Tax Authority (FTA), maintain proper accounting records, and file annual corporate tax returns.

The absence of separate legal personality does not remove corporate tax obligations.

Registration, Filing, and Compliance Obligations

Individuals conducting licensed business activities must register for corporate tax through the EmaraTax portal. They are required to maintain financial records that support the calculation of taxable income and submit corporate tax returns within prescribed deadlines.

Administrative compliance is mandatory even where tax liability is limited or nil. Failure to meet registration or filing requirements may attract penalties under the corporate tax framework.

Situations Where Corporate Tax Does Not Apply

Corporate tax does not apply to individuals earning income solely in their personal capacity without conducting a licensed business activity. Employment income, dividends, capital gains, and personal investment income remain outside the scope of taxation at the individual level.

The critical test is whether the income arises from a licensed commercial or professional activity carried out in the UAE.

Strategic Considerations for Independent Professionals

Freelancers and sole establishment owners should periodically assess whether their activities fall within the corporate tax framework, particularly as revenue grows or operations expand. Monitoring taxable income thresholds, maintaining accurate financial records, and evaluating eligibility for relief provisions are essential compliance steps.

As the UAE’s corporate tax regime continues to evolve, proactive tax planning and regulatory alignment will be critical for independent professionals seeking to manage exposure effectively while sustaining business growth.